One of the big benefits of securing your legacy with the AIS Triangle™, is that it’s like having your own bank.

You can borrow money from your policy. Then you can use it to pay for big-ticket items such as cars or vacations. You can also use it to make investments and start small businesses.

Not only is taking loans from your policy extremely easy and convenient, but as I’m going to explain, by using policy loans to finance your expenses and investments, you can create a positive cash flow that’s potentially worth millions of dollars over a lifetime. We call it “supercharging” your policy.

But before I explain how it works, there is one very simple—but very important— concept you need to understand.

It’s the law of uninterrupted compounding.

Compounding is a simple investment strategy in which you put your money in an investment that pays interest. At the end of the year, you take the interest you earned and reinvest it with your original stake. Now your interest earns a return as well. The next year, you’ll get a bigger interest payment. Then you reinvest that payment, and so on...

A snowball is the best analogy for compounding. As you roll the ball through the snow, the surface area gets bigger. The more surface area on the snowball, the more snow it picks up. The snowball gains mass slowly at first... But pretty soon you can’t move it because it’s so huge.

Compounding is slow and boring at first. But gradually, the interest you earn grows and your reinvestments increase. And the longer you allow your money to compound uninterrupted, the more it grows.

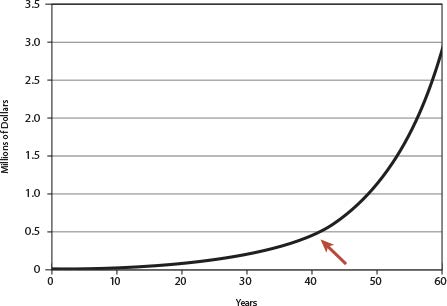

The key to compounding is to let it work over many years. The chart below shows the value of an account when we grow it at 10% per year over 60 years. We call this the “hockey stick” chart, because the money grows slowly for several decades and then really picks up speed after about 40 years.

The Hockey Stick

If you don’t interrupt it, compounding produces a fortune.

At 10% interest, it takes 40 years for $10,000 to grow into $411,000 (see the red arrow). That’s pretty good. But do you see what happens next? The growth of the account explodes.

By year 50, it’s grown to just over $1 million.

By year 60, it’s grown to more than $3 million.

In short, the power of compounding is most effective when you let it work over many decades.

Interrupting the Compounding Process

The compounding process works only if you don’t interrupt it... i.e., you don’t pull money out of the account along the way.

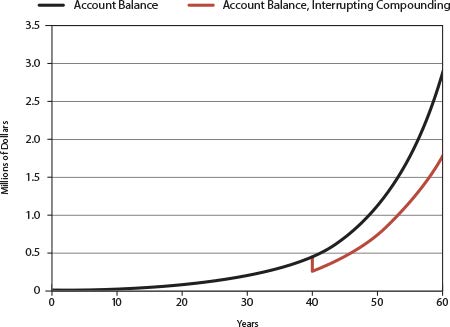

The chart below shows what happens if you make an early withdrawal and pull $150,000 out of your account in year 40.

As you can see, first, the balance in your account drops. That’s the red line you see dipping below the black line. Second, there’s less money in the account to produce interest. You’ve interrupted the compounding.

Look what it does to your wealth...

In year 50, you’ve got $713,000, instead of $1 million. And by year 60, you’re left with $2 million, instead of $3 million. Your account balance is $1 million less in year 60.

Interrupted Compounding

One small withdrawal causes your wealth to plummet.

Thirty-, 40-, and 50-year periods are long. They’re hard for most people to fathom. But we use these time frames to illustrate one important point.

Interrupting the compounding process by liquidating part or all of your funds in the single biggest destroyer of wealth.

These interruptions are not always easy to spot.

For example, a decline of 20% in the stock market interrupts the compounding process in your 401(k) account. That’s because your account balance dropped by 20%. And you have less money producing interest.

You could cash out part of your 401(k) or IRA to buy a new car or house or to give a gift.

That interrupts compounding as well.

Or consider your child’s college fund. You start putting money into it when your child is born. It compounds and grows tax-free in a Coverdell or 529 Plan.

But when your child reaches college age, you liquidate the account to pay for tuition expenses. You’ve interrupted the compounding process after only 18 years.

The Holy Grail of Finance

You know leaving your money alone and letting it compound produces great wealth. But there’s one downside to this: You can’t touch or access your money for a long time.

That’s because you’ll interrupt the compounding.

The holy grail of finance is a vehicle or account that relentlessly compounds your money. But at the same time, it lets you access your money without interrupting the compounding process.

Does such an account exist?

Dividend-paying whole life insurance—the kind we use with the AIS Triangle™—offers us these exact benefits. We put money in one of these policies, and it compounds for the rest of our lives. We capture the power of uninterrupted compounding, and we get rich. Pretty simple, right?

But what if we want to pay for a vacation? Or a car? Or college tuition? Wouldn’t that interrupt compounding?

If this money were in a bank account, a brokerage account, or a 401(k)... yes, it would. When you pay for a big expense, you’d need to liquidate your savings account. Or sell your stocks. Or get rid of your mutual funds.

Doing this would free up your money for use. But, of course, the money is no longer working for you. You’ve interrupted the compounding process. Actually, it’s worse than that: Not only have you stopped the power of compounding, you’ve decreased the value of your savings, stocks, or mutual funds. This results in a critical blow to your long-term returns.

I want to illustrate this visually for you. Below is a rough graphical representation of what most people do as they save for—and then pay for—big-ticket expenses.

First, you save up, earning interest along the way. Those are the green lines. Then you liquidate your account to buy something... maybe a car. You save up. You liquidate. You always end up at zero.

Saving up for Big Purchases

By paying cash for your big-ticket items, you interrupt the compounding process.

But with the AIS Triangle™, you can still pay for these things AND compound your money uninterrupted.

How is this possible?

You save up money in your Vault AIS™ life policy. But at any given time, the insurance company lends you the money you need (up to the amount you’ve saved in your policy). And you pay it back to the insurance company at your own pace. Remember, you can get these loans in under a week with no credit check and no 30-page application.

The insurance company is willing to do this because it has nothing to lose. Even if you decide not to pay back the loan, the insurance company could simply deduct whatever you owe from your payout when you die.

In short, because of the policy loan feature and the guaranteed lending provision that comes with your Vault AIS™ policy, if you need money, you can borrow it from the insurance company. And because you use the company’s money, nothing interrupts the compounding of the money in your policy.

Remember our uninterrupted compounding chart from earlier? Here it is again.

The Hockey Stick

The path our money is taking in an Income for Life policy.

Let’s look at what happens when you use your Vault AIS™ life policy to buy something. Remember, when you borrow from your Vault AIS™ life policy to make a purchase, you don’t liquidate your savings, your brokerage account, your IRA, or your college plan as you did with our earlier example. You take a policy loan from the insurance company and repay it over time.

Because you took out a loan and used the insurance company’s money, your money continued to compound and grow... uninterrupted.

Now, five years later, you’ve repaid your policy loan. But the cash value balance in your policy is much higher because you let it compound uninterrupted.

By using a series of loans to pay for life’s big expenses, you will never interrupt the compounding process.

The illustration below shows you how this process looks. The black line is a close-up of the “hockey stick” compounding curve. The green dots represent points in time at which you might take policy loans. The green lines represent your shrinking loan balance each year as you pay back your loans

The Path to Uninterrupted Compounding

Use policy loans to pay for your big-ticket items.

In short, by borrowing money from the insurance company, you can continue compounding within your policy even as you spend.

Recap

To summarize, we’ve shown you how devastating the action of interrupting the compounding process is. And we’ve shown you how the average person destroys his or her wealth by doing this many times throughout life.

Vault AIS™ Secured by the AIS Triangle™, is the only solution I know of that allows you to harness the power of uninterrupted compounding... but still lets you spend your money when you need it. This is a difficult concept for many to grasp. And we’re sure you’ll have more questions.

There’s still a lot of ground to cover, including specific examples of using policy loans for cars, vacations, college expenses, etc. And we’ll cover the right strategy for paying your loans back.

In Prosperity,

Michael G Isom

P.S. Borrowing money from banks, credit card companies, and other lenders is the most damaging thing you can do to your wealth. When you take a loan to finance a purchase, you start in the hole and have to claw your way back to zero, paying interest to the bank along the way. And you’ll never get ahead (see the chart below).