Imagine never running out of money in retirement. What would that feel like?

When someone thinks of saving or investing money, they usually think of the stock market; and for most people they are investing in a 401(k), IRA, stocks, or mutual funds. The traditional ideas of saving and investing for retirement are ideas that are usually tied to the stock market. This is extremely prevalent in the financial planning world.

Notice the first circle below. This circle represents one pool of money – stock market money; 401(k)’s, IRA’s, mutual funds, stocks, and bonds

When someone is saving or investing in the stock market, and only in this one pool of money for their entire working life, even through retirement, every dollar going into this pool of money is subject to interest rates, or a rate of return. It doesn’t matter if it’s bonds or stocks or mutual funds, that pool of money is relegated to interest rates for a lifetime…and subject to volatility. There are no guarantees.

Now, think about that. When someone retires they have built up this net worth; this Nest Egg, this pool of money. They now start taking income from that pool of money in retirement.

What happens in a down year? What did people do in 2008 when the market crashed but they still needed income from their investments? They had to take money from that down account, adding insult to injury.

They are now taking income from an account that has lost value; and in some cases 30%, 40%, 50% value lost. They are taking income from that negative account.

So, it’s extremely painful and it erodes the account even further when you have to take income in a down year, or after a down year.

Here’s how cash value insurance comes into play. You are able to create a second pool of money through a whole life insurance policy that is not subject to loss. This pool of money is not tied to the stock market. It is based on actuarial science and cash value guarantees.

Your money is guaranteed to grow. There are no losses. There are no “down” years.

We only recommend mutual life insurance companies that have been around for over 130 years. They use what’s called actuarial science; they know when people are going to pass away and they use that knowledge and data to create guarantees and dividends. Because of that, they are profitable and those profits go back to policy holders, you and me, which is a good thing.

Because this second pool of money is not tied to what the stock market is doing, you have an opportunity for more certainty in your financial plan; for more predictability.

Imagine having this second pool of money in your financial portfolio and there is a stock market crash. You don’t have to take money from the stock market account that is down 30% or 40%. You can now take your income from the cash value of your whole life insurance policy. Imagine the peace of mind that that can bring; knowing that in a down market you don’t have to add “salt to the wound” by taking out income from a negative account. You can now shift over and take that income from the cash value whole life policy.

So, let’s look at the numbers and see how that actually works.

Below is a cash flow calculator. We want to look at this illustrated over a 25 year time frame. Let’s assume you retire at the age of 65. You live another 25 years and you have a pool of money that you have accumulated in the stock market. This lump sum is your Net Worth or your Nest Egg. And just for round numbers sake let’s use $1,000,000 because it’s easy to think about.

Many financial advisers believe the stock market has averaged 10% to 12% returns, that’s not reality, but let’s look at that number to make a point.

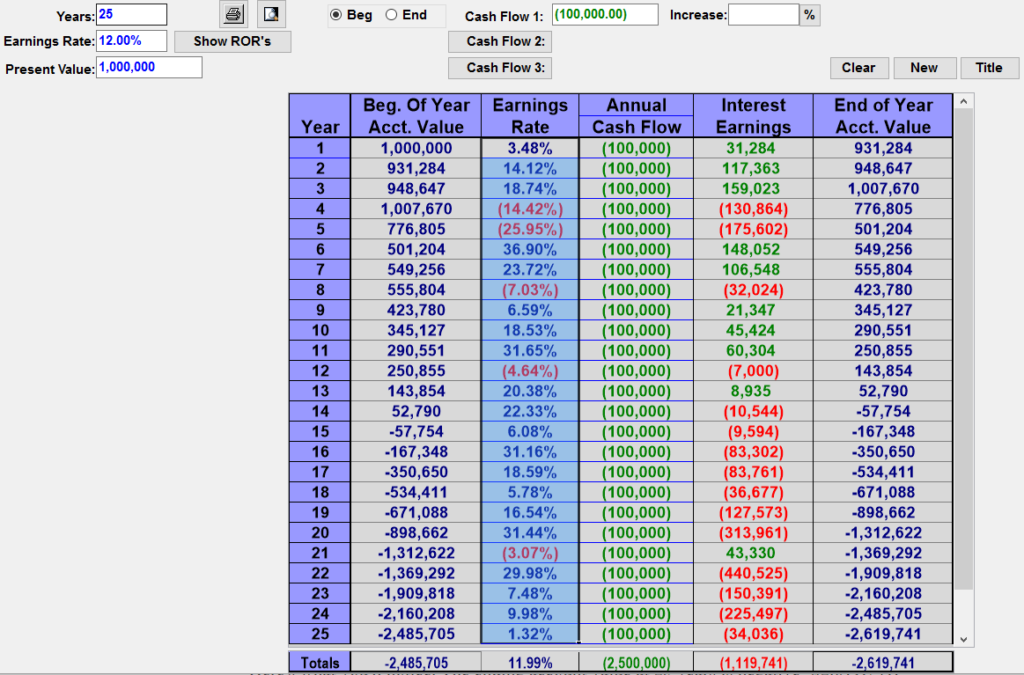

So here you see market history. I’ve chosen a time frame from 1970 to 1994 which is 25 years, and I’m going to use the 11.99% return and round up to 12% for our example. This is a 12% Average Rate of Return.

Notice, this is the S&P 500 with Dividends. Which keep in mind, most investors don’t get the dividends, those dividends go back to money managers. So, this isn’t reality, but I’m going to use it for my example today.

12% – It would seem to make sense then that by only living off of 10% a year that you could do that and not run out of money. That if you were earning 12% and only living off of 10% that you would be fine. Well, 10% of $1,000,000 is $100,000. So, this is your income, $100,000 per year. This is coming from your stock market portfolio.

Look at the chart and it looks like after 25 years you would be able to spend $2,500,000 and still have left $2,066,671 that you can leave to beneficiaries, family or a charity as a legacy. It all looks really nice, but, this isn’t reality.

Let’s take the actual returns, not the average returns, and put them into the calculator. Because notice, the market doesn’t really do 12% every single year as we see in the “Earnings Rate” column. Again, 12% is the average return, but the actual 25 year history is what we’ll paste into the chart, which includes the good years and the bad years.

Here’s what you’ll notice in the chart below. The ending account value at 25 years is negative -$2.619,741. We can’t even go there. Once you’re out of money, you’re out of money, you can’t go to negative -$2.619,741.

What happened? We see in “Year 1” you would have been able to pull the $100,000 of income, but look at “Year 4”. The market is down 14.42% and you pull $100,000, your losses are compounded. You lose $130,864. The next year is even worse. The market is down nearly 25.95%. You still need income, so you pull the $100,000 from the market portfolio, adding insult to injury, now you suffer substantial losses of $175,602.

Five years have gone by and because of market losses and the need for $100,000 of income, the Account Value has dropped from $1,000,000 to only $501,204…Ouch.

As you can see here, it’s very painful to be pulling income from a down account. You run out of money after the 13th year.

This is where the cash value life insurance comes into play. You can use it as a “buffer”. I want you to think about this. The cash value in your whole life insurance policy becomes a part of your portfolio. You now have a buffer. This is one option of many options that whole life brings to the table, it’s not the only option.

Having the cash value life insurance in your financial portfolio gives you many more options that you otherwise simply wouldn’t have had.

Remember, cash value whole life is not tied to the stock market. Your money is guaranteed to grow, year after year.

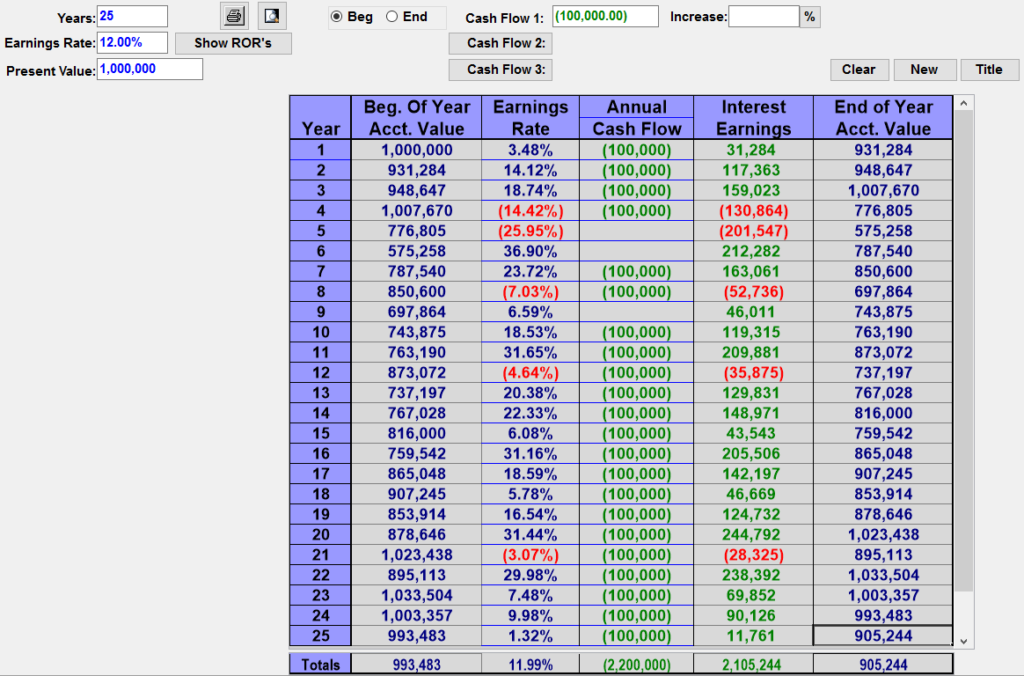

The rule of thumb for using cash value in retirement combined with investments is this. While having the cash value whole life in your portfolio, you’re pulling income from your stock market investments, the year after a down year in your investment account, you’re going to take income from the life insurance policy. Because in a down year, you don’t know that the year is going to be down. So, you look 12 months back and you see that you’ve lost 14.42%. You now take your income from the policy. So, in year 5 instead of pulling $100,000 from the stock market investment, you’re going to pull that $100,000 from the cash value of your life insurance.

Year 5 was a down year also, so in year 6 you don’t pull money from the stock market investment. In year 7 you now pull from the stock market portfolio. Year 8 was a down year, so in year 9 you pull the $100,000 from the policies cash value. And then in year 10 you’re to pulling the $100,000 income from the stock market investment.

Here’s what that looks like:

We only used the life insurance buffer three times; year 5, year 6, and year 9. But look what those 3 times did. You were still able to pull $2,200,000 from the stock market investments, plus an additional $300,000 from the life insurance policy and you still have $905,000 in the investment that you can leave as a legacy. Plus there can also be a life insurance death benefit that can pass tax-free to heirs.

The point is this, by having the cash value life insurance in your portfolio, you were able to buffer against the stock market crashes and those down years of the market. This is just one benefit of cash value insurance. There are many others. Cash value whole life can be used as a buffer in your portfolio.

There’s more predictability and certainty in your financial plan. You don’t have to relegate yourself to all stock market investments and what the interest earnings may, or may not be. You can create this second pool of money for safety, for liquidity, for certainty and peace of mind.

Continue to educate yourself on the tremendous benefits of cash value life insurance. Learn more and discover how you can expand your personal income in retirement and what this will do for you.