In this technical analysis we are going to look at the true cost of owning a home over a 30 year period of time.

Have you ever heard that you pay less interest on a 15 year mortgage versus a 30 year? Did you stop there concluding that since you are paying less interest it must be more efficient?

Why would a financial institution incentivize us with a slightly lower interest rate on a 15 year vs. a 30 year?

Is having a lower payment on the 30 year a good hedge against inflation?

Could you save the difference between a 15 year and a 30 year payment and pay the home off at any time you wanted in the future?

Is one of your goals in your overall financial plan to save on taxes for as long as you can? And in the most efficient way?

What are your biggest personal tax deductions that you take?

- Could they be your mortgage interest deduction?

- Kids as dependents?

- Charitable contributions?

Below you will see a recent analysis I did for a client on a $350,000 mortgage.

We are measuring it over a 30 year period of time.

- What is the cost if you pay cash?

- What is the cost if you do a 15 year mortgage?

- What is the cost if you do a 30 year mortgage?

A $350,000 mortgage comparison measured over 30 years.

When we look at a mortgage, the first thing to consider is the amount of money out of pocket that we pay towards the mortgage.

- If we pay cash it’s $350k out of pocket.

- If it’s a 15 year loan, 180 months divided by $350k is $1,944.44/mo. ($1944.44 X 180 = $350k out of our pocket)

- 30 year, 360 divided by $350k is $972.22/mo.

Thus 350k total amount out of pocket over the 30 year period of time; whether we pay cash, do a 15 year or 30 year. The amount of money out of our pocket is the same assuming no interest on paying cash, 15 or 30 year.

The only variable I added to this calculator is 4% on the loan rate for both.

This takes the 15yr. payment to $2,588.91/mo. and the 30yr. to $1,670.95/mo.

Now we are measuring the lost opportunity cost on paying cash, a 15 yr. and a 30 yr. with the amount of money that actually comes out of our pocket that is paid toward the home.

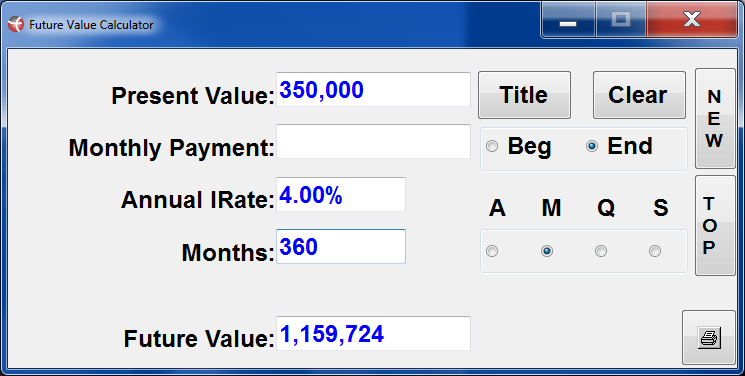

You can see here that if we left the 350k in an account earning 4% it would compound out to $1,159,724. That then represents the opportunity cost of paying cash with a 4% cost of money.

The true cost of paying cash today at 4% opportunity cost over 30 years is $1,159,724.

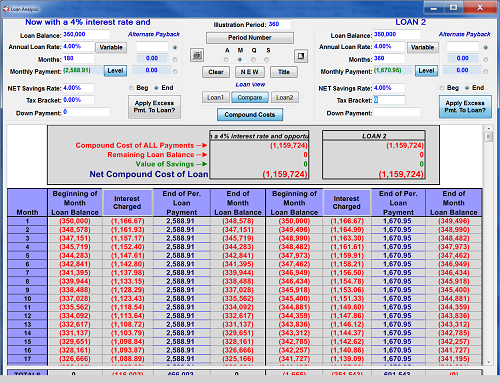

This next calculator shows the 4% added to each loan and also the opportunity cost.

So the only variable that was changed was 0 on interest before and now it is 4. This now helps us see that every dollar out of our pocket is costing us 4% a year totaling up to the $1,159,724.

If we pay cash, 15 or 30 year, the amount of money out of our pocket is the same at 4% opportunity cost.

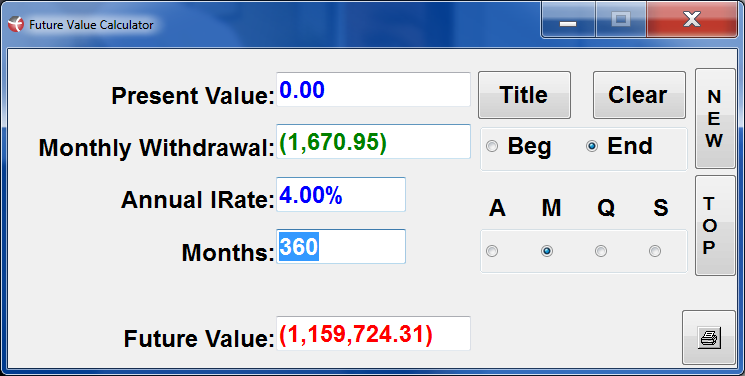

This shows the monthly payment on the 30yr. loan at a 4% opportunity cost totaling the $1,159,724.

The calculator above shows the 15yr. payment at 4% opportunity cost for the first 180 months paid totaling an opportunity cost of $637,106.

We then need to take that opportunity cost of $637,106 and compound that cost at 4% for the next 15 years or 180 months.

See the calculator below showing the $637k in 180 months growing to the $1,159,724 from 180 months to 360 months.

- Remember we are measuring this over 360 months even though the home is paid for in 180 months, the opportunity cost continues for the next 180 months.

Then we add in the tax savings which makes the 360 month or 30 year the most efficient, economically speaking.

We have concluded that you pay the same amount of money out of your pocket. The opportunity cost is the same. The difference is that on a 30 year mortgage the interest write-off lasts longer. This tax savings over a longer period of time is what makes owning a 30 year mortgage more efficient.

- Paying $350,000 cash for a home at a 4% opportunity cost over a 30 year period of time = $1,159,274

- Doing a 15 year mortgage, measuring it over a 30 year period of time has a net cost of $1,071,727

Along with a host of other benefits we talked about a 30yr. loan is a much smaller payment, this frees up cash to save, keeps our payment lower to hedge against inflation – everything else is inflating and our mortgage payment stays the same.

When we save the difference between the 15yr. or 20yr. loan and the 30yr. loan we can build up reserves for liquid safety net/security to fall back on if ever needed.

Also, it could be saved and used to build other assets that you may want to accomplish – income producing assets and a personal cash flow banking system.

I hope this helps when considering an overall financial strategy and how a personal mortgage plays into it.

Sincerely,

Michael Isom

Owner of Optic Financial & Creator of the 20/20 Personal Banking System